The Child Tax Credit and the Child and Dependent Care Tax Credit — Understanding the Difference

Overview

- The Child and Dependent Care Tax Credit (CDCTC) helps working parents offset the cost of child care and gives them the flexibility to choose the type of care that best meets their needs.

- The Child Tax Credit (CTC) helps families cover a wide range of expenses associated with raising a child, including food, rent, clothes, medicine, diapers, etc. It plays an important role in helping to lift families out of poverty.

- In 2025, both the CDCTC and the CTC were permanently expanded as part of the tax reconciliation package (H.R. 1).

- As parents face rising costs for basic goods and services, including child care, both credits are essential. Together they support families and build pathways to long-term economic stability.

The Child and Dependent Care Tax Credit and the Child Tax Credit support families in different ways. Families need both.

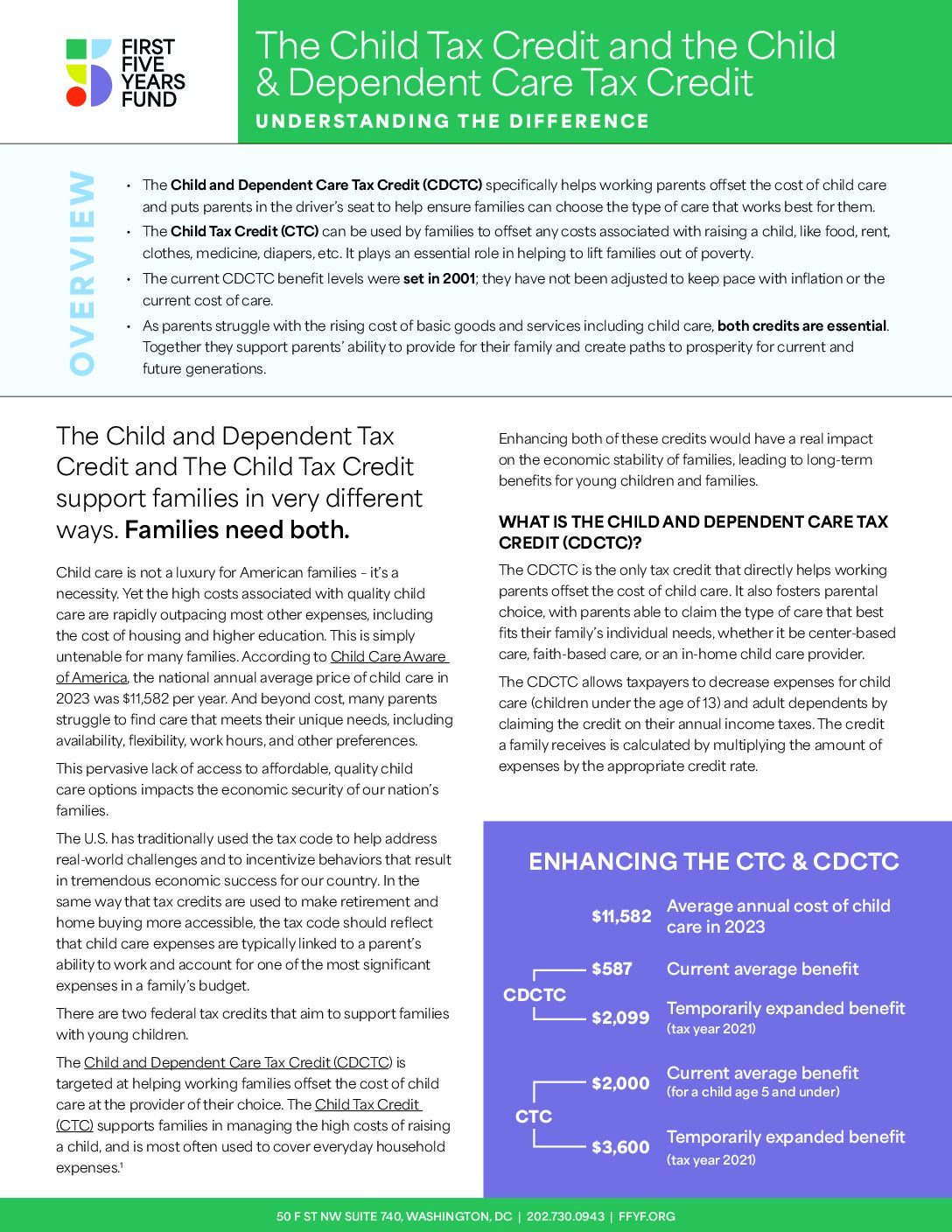

Child care is not a luxury for American families – it’s a necessity. Yet the cost of quality child care is rising faster than most other expenses, including housing and higher education. For many families, this is simply untenable.

According to Child Care Aware of America, the national average annual price of child care in 2025 was $13,184 per year. Beyond cost, many parents also struggle to find care that meets their needs, including factors such as affordability, convenience, size, hours, setting, etc.

This widespread lack of access to affordable, quality child care undermines the economic security of families across the country.

The U.S. has long used the tax code to address real-world challenges and incentivize behaviors that drive economic growth. Just as tax credits help make retirement savings and homeownership more accessible, the tax code should also recognize that child care is essential to a parent’s ability to work and represents one of the largest expenses in a family’s budget.

Subscribe to FFYF First Look

Every morning, FFYF reports on the latest child care & early learning news from across the country. Subscribe and take 5 minutes to know what's happening in early childhood education.

Related

New Joint Economic Committee (JEC) Minority Report Highlights Impact of Child Care Tax Credits

Existing child care tax incentives are a tool that can reduce child care costs for families while delivering a strong return on investment for employers.

The Child and Dependent Care Tax Credit: How It Works

The Child and Dependent Care Tax Credit (CDCTC) is the only tax credit specifically designed to help families offset the costs of child care while they work, attend school, or look for work.

Toolkit: Child Care Tax Credits

The tools you need to highlight how child care tax credits help make care more accessible and affordable for families nationwide.