The Child and Dependent Care Tax Credit: How It Works

Overview

The Child and Dependent Care Tax Credit (CDCTC) is the only tax credit specifically designed to help families offset the costs of child care while they work, attend school, or look for work. The credit helps millions of families each year cover a portion of their child care costs by allowing parents to claim a percentage of qualifying child care expenses on their annual tax return. Because the CDCTC is non-refundable, taxpayers must have earned income to receive the credit.

Updated in July 2025, the CDCTC helps make child care more affordable for working families with young children while giving parents the flexibility to choose the care arrangement that best meets their needs. In 2022, more than 5.7 million families nationwide benefited from this important tax credit.

State Examples

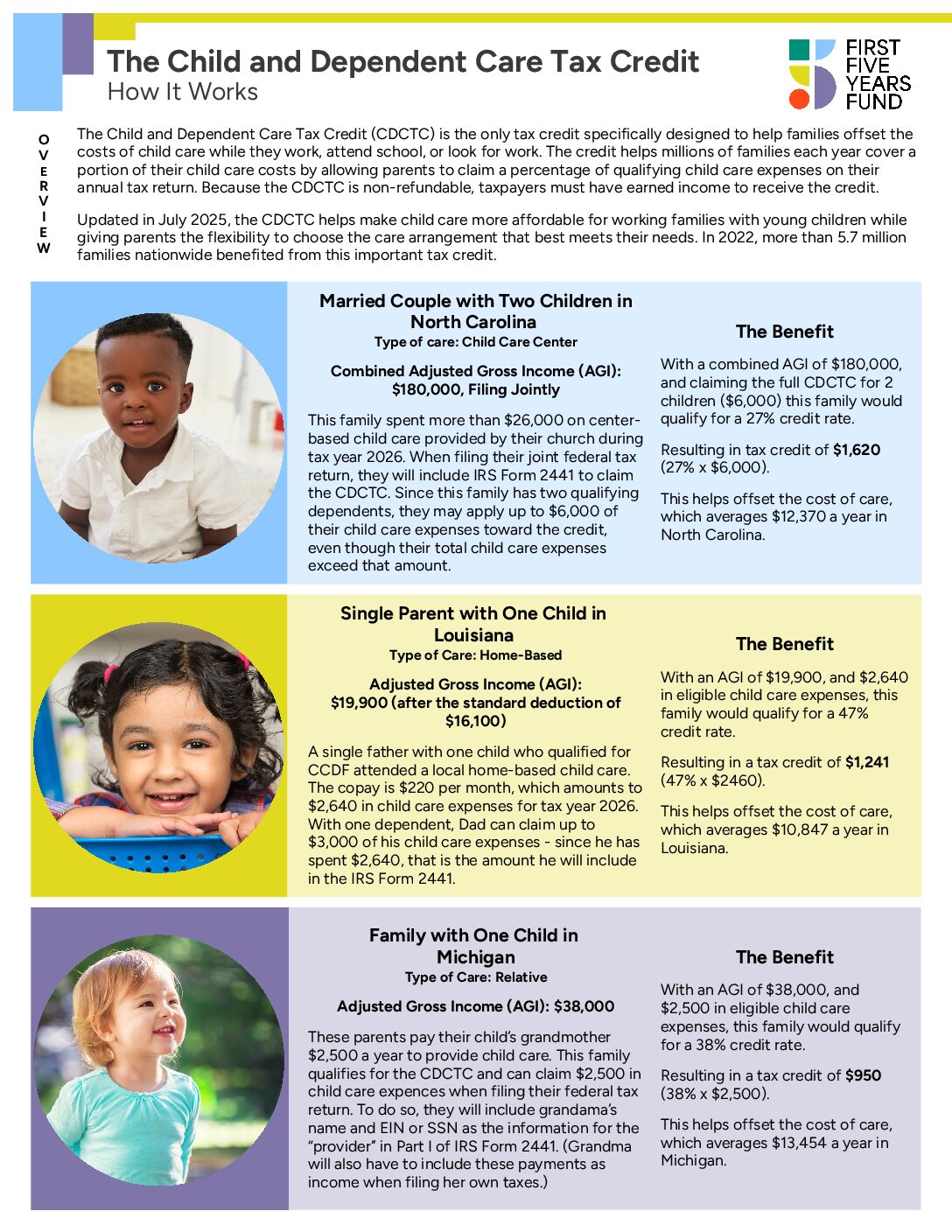

Married Couple with Two Children in North Carolina

Type of care: Child Care Center

Combined Adjusted Gross Income (AGI): $180,000, Filing Jointly

This family spent more than $26,000 on center-based child care provided by their church during tax year 2026. When filing their joint federal tax return, they will include IRS Form 2441 to claim the CDCTC. Since this family has two qualifying dependents, they may apply up to $6,000 of their child care expenses toward the credit, even though their total child care expenses exceed that amount.

The Benefit

With a combined AGI of $180,000, and claiming the full CDCTC for 2 children ($6,000) this family would qualify for a 27% credit rate.

Resulting in tax credit of $1,620 (27% x $6,000).

This helps offset the cost of care, which averages $12,370 a year in North Carolina.

Single Parent with One Child in Louisiana

Type of Care: Home-Based

Adjusted Gross Income (AGI): $19,900 (after the standard deduction of $16,100)

A single father with one child who qualified for CCDF attended a local home-based child care. The copay is $220 per month, which amounts to $2,640 in child care expenses for tax year 2026. With one dependent, Dad can claim up to $3,000 of his child care expenses – since he has spen

The Benefit

With an AGI of $19,900, and $2,640 in eligible child care expenses, this family would qualify for a 47% credit rate.

Resulting in a tax credit of $1,241 (47% x $2460).

This helps offset the cost of care, which averages $10,847 a year in Louisiana.

Family with One Child in Michigan

Type of Care: Relative

Adjusted Gross Income (AGI): $38,000

These parents pay their child’s grandmother $2,500 a year to provide child care. This family qualifies for the CDCTC and can claim $2,500 in child care expences when filing their federal tax return. To do so, they will include grandama’s name and EIN or SSN as the information for the “provider” in Part I of IRS Form 2441. (Grandma will also have to include these payments as income when filing her own taxes.)

The Benefit

With an AGI of $38,000, and $2,500 in eligible child care expenses, this family would qualify for a 38% credit rate.

Resulting in a tax credit of $950 (38% x $2,500).

This helps offset the cost of care, which averages $13,454 a year in Michigan.

How It Works

The Child and Dependent Care Tax Credit (CDCTC) allows parents to claim up to $3,000 in eligible child care expenses for one child or up to $6,000 for two or more children. The amount parents receive depends on their income; the lower the income, the higher the percentage of expenses they can claim as a tax credit. The credit then reduces the amount of federal taxes the owed.

To claim the CDCTC, the filer must complete Part I and Part II of IRS Form 2441. Part III only needs to be completed if the parent received dependent care benefits during the same tax year.

To complete the form, the filer provides the following information:

Part I – Persons or Organizations Who Provided the Care

- Columns (a) – (c): The care provider’s name, address, employer identification number (EIN) or social security number (SSN)

- Column (d): Whether or not the care provider was a household employee

- Column (e): The amount paid to all persons/organizations who provided care

Part II – Credit for Child and Dependent Care Expenses

- Columns (a) and (b): Each qualifying dependent’s first and last name and social security number

- Column (d): The amount of qualified care expenses paid for each dependent

- Line 3: The combined amount from Column (d) that does not exceed $3,000 for one dependent or $6,000 for two or more dependents

- Lines 4 and 5: The filer’s earned income and, if married filing jointly, the spouse’s earned income

- Line 11: The total credit amount, calculated by multiplying the number in Line 3 by the credit rate listed for the filer’s income bracket

Relative Care

Families paying a relative to help care for their children are also eligible for the CDCTC. The relative must be a grandparent, aunt/uncle, adult sibling, or cousin.

The process is the same as claiming CDCTC in a more formal child care arrangement:

- The family must complete IRS Form 2441, including providing an EIN or SSN for the relative

- The relative must also report these payments as income on their own tax return

- If these payments are over $2,700 in a year or more than $1,000 in a quarter, the family will also need to consider payroll taxes – payments under this amount are exempt from payroll taxes

Learn More

- Overview: Child & Dependent Care Tax Credit

- State-By-State: A Look At How Many Families Receive the Child and Dependent Care Tax Credit (CDCTC)

- Child and Dependent Care Tax Credit (CDCTC): Maximum Credit Amounts for Families

For More Information: Amanda Guarino, aguarino@ffyf.org

Download

Subscribe to FFYF First Look

Every morning, FFYF reports on the latest child care & early learning news from across the country. Subscribe and take 5 minutes to know what's happening in early childhood education.

Related

New Joint Economic Committee (JEC) Minority Report Highlights Impact of Child Care Tax Credits

Existing child care tax incentives are a tool that can reduce child care costs for families while delivering a strong return on investment for employers.

The Child Tax Credit and the Child and Dependent Care Tax Credit — Understanding the Difference

Overview The Child and Dependent Care Tax Credit and the Child Tax Credit support families in different ways. Families need both. Child care is not a luxury for American families …

Toolkit: Child Care Tax Credits

The tools you need to highlight how child care tax credits help make care more accessible and affordable for families nationwide.